Printable PDF

Printable PDFCPA-REGULATION Exam Questions & Answers

Vendor: Test Prep

Certifications: Test Prep Certifications

Exam Code: CPA-REGULATION

Exam Name: CPA Regulation

Updated: Jul 06, 2026

Q&As: 69 ( View Details)

Note: Product instant download. Please sign in and click My account to download your product.

The CPA-REGULATION Questions & Answers covers all the knowledge points of the real exam. We update our product frequently so our customer can always have the latest version of the brain dumps. We provide our customers with the excellent 7x24 hours customer service. We have the most professional expert team to back up our grate quality products. If you still cannot make your decision on purchasing our product, please try our free demo.

Download Free Test Prep CPA-REGULATION Demo

Experience

Pass4itsure.com exam material in PDF version.

Simply submit your e-mail address below to get

started with our PDF real exam demo of your

Test Prep CPA-REGULATION exam.

![]() Instant download

Instant download

![]() Latest update demo according to real exam

Latest update demo according to real exam

* Our demo shows only a few questions from your selected exam for evaluating purposes

- Q&As Identical to the VCE Product

- Windows, Mac, Linux, Mobile Phone

- Printable PDF without Watermark

- Instant Download Access

- Download Free PDF Demo

- Includes 365 Days of Free Updates

VCE

- Q&As Identical to the PDF Product

- Windows Only

- Simulates a Real Exam Environment

- Review Test History and Performance

- Instant Download Access

- Includes 365 Days of Free Updates

CPA-REGULATION Online Practice Questions and Answers

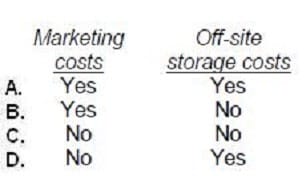

Under the uniform capitalization rules applicable to property acquired for resale, which of the following costs should be capitalized with respect to inventory if no exceptions are met?

A. Option A

B. Option B

C. Option C

D. Option D

DAC Foundation awarded Kent $75,000 in recognition of lifelong literary achievement. Kent was not required to render future services as a condition to receive the $75,000. What condition(s) must have been met for the award to be excluded from Kent's gross income?

I. Kent was selected for the award by DAC without any action on Kent's part.

II.

Pursuant to Kent's designation, DAC paid the amount of the award either to a governmental unit or to a charitable organization.

A.

I only.

B.

II only.

C.

Both I and II.

D.

Neither I nor II.

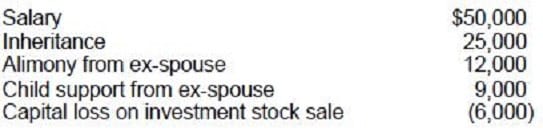

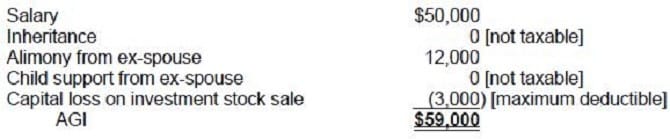

In the current year Jensen had the following items:

What is Jensen's AGI for the current year?

A. $44,000

B. $59,000

C. $62,000

D. $84,000

What Our Customers Are Saying

Roger

United StatesAs for me , this dumps is very useful and convenient, I can find my disadvantages easily and know how to correct them. I also can learn new skills and knowledge by using this dumps. I think you also can do it. I have test it so you can trust on it.

Nebeker

South AfricaThis dumps is very valid and is enough to your exam, so just trust on it and do it carefully.

Zouleha

United StatesUpdate quickly and be rich in content,this dumps is really valid. Thanks.

Younan

SwitzerlandPassed this exam with a score of 941.Most of them are in this dumps.

August

PakistanThis dumps is valid, and this dumps is the only study material i used for this exam. Surprisingly i met the same question in the exam, so i passed the exam without doubt. Thanks for this dumps and i will recommend it to my friends.

Pasi

Australiatook the exams yesterday and passed. I was very scared at first because the labs came in first so I was spending like 10 to 13mins so I started rushing after the first three labs thinking that I will have more labs. I ended up finishing the exam in an hour.. dumps are valid.

Galen

Luxembourghi guys, i passed this exam today. all the questions with correct answers in this dumps. recommend.

Quinley

PakistanThis Dump is Valid.I gave my test today, and passed,thanks!

Lisy

Thailandtoday i'm pass the exam with high score. believe on it.

Banne

Nigeriatook the exams yesterday and passed. I was very scared at first because the labs came in first so I was spending like 10 to 13mins so I started rushing after the first three labs thinking that I will have more labs. I ended up finishing the exam in an hour..d dumps are valid. I tink there is a new lab. good success

Home | Contact Us | About Us | FAQ | Guarantee & Policy | Privacy & Policy | Terms & Conditions | How to buy

Copyright © 2026 pass4itsure.com. All Rights Reserved