CPA-REGULATION Online Practice Questions and Answers

In which of the following situations may taxpayers file as married filing jointly?

A. Taxpayers who were married but lived apart during the year.

B. Taxpayers who were married but lived under a legal separation agreement at the end of the year.

C. Taxpayers who were divorced during the year.

D. Taxpayers who were legally separated but lived together for the entire year.

Conner purchased 300 shares of Zinco stock for $30,000 in 1980. On May 23, 1994, Conner sold all the

stock to his daughter Alice for $20,000, its then fair market value. Conner realized no other gain or loss

during 1994. On July 26, 1994, Alice sold the 300 shares of Zinco for $25,000.

What was Alice's recognized gain or loss on her sale?

A. $0

B. $5,000 long-term gain.

C. $5,000 short-term loss.

D. $5,000 long-term loss.

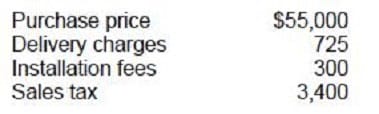

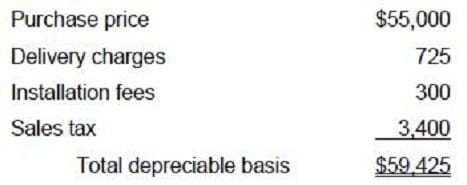

Starr, a self-employed individual, purchased a piece of equipment for use in Starr's business. The costs associated with the acquisition of the equipment were:

What is the depreciable basis of the equipment?

A. $55,000

B. $58,400

C. $59,125

D. $59,425

Gibson purchased stock with a fair market value of $14,000 from Gibson's adult child for $12,000. The child's cost basis in the stock at the date of sale was $16,000. Gibson sold the same stock to an unrelated party for $18,000. What is Gibson's recognized gain from the sale?

A. $0

B. $2,000

C. $4,000

D. $6,000

Cobb, an unmarried individual, had an adjusted gross income of $200,000 in 1990 before any IRA deduction, taxable social security benefits, or passive activity losses. Cobb incurred a loss of $30,000 in 1990 from rental real estate in which he actively participated. What amount of loss attributable to this rental real estate can be used in 1990 as an offset against income from nonpassive sources?

A. $0

B. $12,500

C. $25,000

D. $30,000

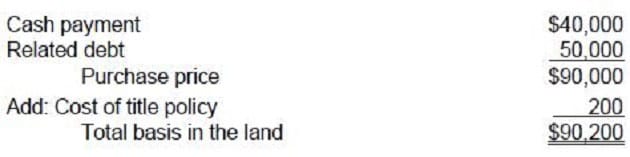

Fred Berk bought a plot of land with a cash payment of $40,000 and a mortgage of $50,000. In addition, Berk paid $200 for a title insurance policy. Berk's basis in this land is:

A. $40,000

B. $40,200

C. $90,000

D. $90,200

For a cash basis taxpayer, gain or loss on a year-end sale of listed stock arises on the:

A. Trade date.

B. Settlement date.

C. Date of receipt of cash proceeds.

D. Date of delivery of stock certificate.

Among which of the following related parties are losses from sales and exchanges not recognized for tax purposes?

A. Father-in-law and son-in-law.

B. Brother-in-law and sister-in-law.

C. Grandfather and granddaughter.

D. Ancestors, lineal descendants, and all in-laws.

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent. Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040. Tom's 1994 wages were $53,000. In addition, Tom's employer provided group-term life insurance on Tom's life in excess of $50,000. The value of such excess coverage was $2,000.

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000

K. $10,000

L. $25,000

M. $50,000

N. $55,000

O. $75,000

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent. Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040. During 1994, the Moores received a $2,500 federal tax refund and a $1,250 state tax refund for 1993 overpayments. In 1993, the Moores were not subject to the alternative minimum tax and were not entitled to any credit against income tax. The Moores' 1993 adjusted gross income was $80,000 and itemized deductions were $1,450 in excess of the standard deduction. The state tax deduction for 1993 was $2,000.

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000

K. $10,000

L. $25,000

M. $50,000

N. $55,000

O. $75,000

Home | Contact Us | About Us | FAQ | Guarantee & Policy | Privacy & Policy | Terms & Conditions | How to buy

Copyright © 2026 pass4itsure.com. All Rights Reserved