FINANCIAL-ACCOUNTING-AND-REPORTING Online Practice Questions and Answers

According to the FASB conceptual framework, the process of reporting an item in the financial statements of an entity is:

A. Allocation.

B. Matching.

C. Realization.

D. Recognition.

During a period when an enterprise is under the direction of a particular management, its financial statements will directly provide information about:

A. Both enterprise performance and management performance.

B. Management performance but not directly provide information about enterprise performance.

C. Enterprise performance but not directly provide information about management performance.

D. Neither enterprise performance nor management performance.

At December 31, 1998, Off-Line Co. changed its method of accounting for demo costs from writing off the costs over two years to expensing the costs immediately. Off-Line made the change in recognition of an increasing number of demos placed with customers that did not result in sales. Off-Line had deferred demo costs of $500,000 at December 31, 1997, $300,000 of which were to be written off in 1998 and the remainder in 1999. Off-Line's income tax rate is 30%. In its 1998 financial statements, what amount should Off-Line report as cumulative effect of change in accounting principle?

A. $0

B. $200,000

C. $350,000

D. $500,000

Lore Co. changed from the cash basis of accounting to the accrual basis of accounting during 1994. The cumulative effect of this change should be reported in Lore's 1994 financial statements as a:

A. Prior period adjustment resulting from the correction of an error.

B. Prior period adjustment resulting from the change in accounting principle.

C. Component of income before extraordinary item.

D. Component of income after extraordinary item.

What is the purpose of information presented in notes to the financial statements?

A. To provide disclosures required by generally accepted accounting principles.

B. To correct improper presentation in the financial statements.

C. To provide recognition of amounts not included in the totals of the financial statements.

D. To present management's responses to auditor comments.

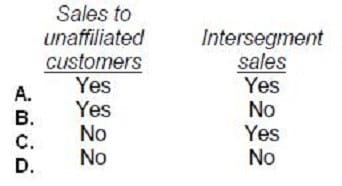

In financial reporting of segment data, which of the following must be considered in determining if an industry segment is a reportable segment?

A. Option A

B. Option B

C. Option C

D. Option D

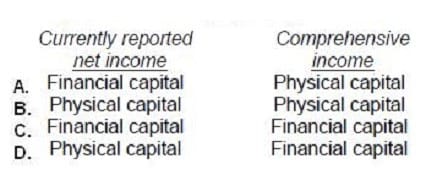

FASB's conceptual framework explains both financial and physical capital maintenance concepts. Which capital maintenance concept is applied to currently reported net income, and which is applied to comprehensive income?

A. Option A

B. Option B

C. Option C

D. Option D

During the second quarter of 1988, Buzz Company sold a piece of equipment at a $12,000 gain. What portion of the gain should Buzz report in its income statement for the second quarter of 1988?

A. $12,000

B. $6,000

C. $4,000

D. $0

YIV, Inc. is a multidivisional corporation, which has both intersegment sales and sales to unaffiliated customers. YIV should report segment financial information for each division meeting which of the following criteria?

A. Segment operating profit or loss is 10% or more of consolidated profit or loss.

B. Segment operating profit or loss is 10% or more of combined operating profit or loss of all company segments.

C. Segment revenue is 10% or more of combined revenue of all the company segments.

D. Segment revenue is 10% or more of consolidated revenue.

Grum Corp., a publicly-owned corporation, is subject to the requirements for segment reporting. In its income statement for the year ended December 31, 1991, Grum reported revenues of $50,000,000, operating expenses of $47,000,000, and net income of $3,000,000. Operating expenses include payroll costs of $ 15,000,000. Grum's combined identifiable assets of all industry segments at December 31, 1991, were $40,000,000. Cott Co.'s four business segments have revenues and identifiable assets expressed as percentages of Cott's total revenues and total assets as follows: Which of these business segments are deemed to be reportable segments?

A. Ebon only.

B. Ebon and Fair only.

C. Ebon, Fair, and Gel only.

D. Ebon, Fair, Gel, and Hak.

Home | Contact Us | About Us | FAQ | Guarantee & Policy | Privacy & Policy | Terms & Conditions | How to buy

Copyright © 2026 pass4itsure.com. All Rights Reserved