CPA-TEST Online Practice Questions and Answers

Which of the following statements is correct concerning significant deficiencies in internal control with respect to an audit of a nonissuer?

A. An auditor is required to search for significant deficiencies during an audit.

B. All significant deficiencies are also considered to be material weaknesses.

C. An auditor may communicate significant deficiencies during an audit or after the audit's completion.

D. An auditor may report that no significant deficiencies were noted during an audit.

Under the Revised Model Business Corporation Act, which of the following must be contained in a corporation's articles of incorporation?

A. Quorum voting requirements.

B. Names of stockholders.

C. Provisions for issuance of par and nonpar shares.

D. The number of shares the corporation is authorized to issue.

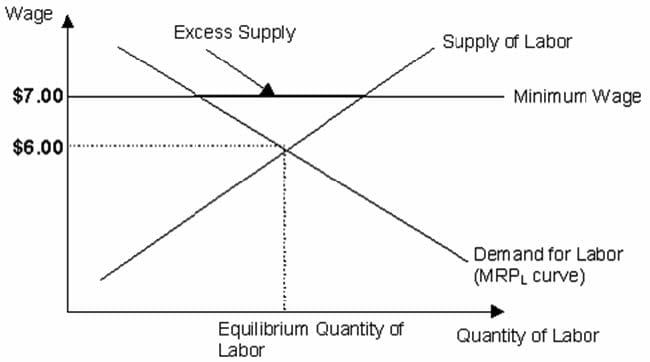

Suppose the equilibrium wage for low skilled workers in California is $6.00 an hour. If the government increases the minimum wage to $7.00 an hour, what would be the effect on the market for low skilled labor?

A. An excess demand for labor would result.

B. An excess supply of labor would result.

C. The demand for labor would decrease.

D. The supply of labor would increase.

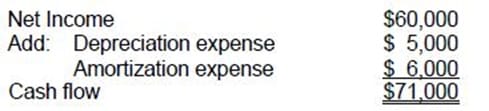

ABC Corporation had income before taxes of $60,000 for the year 1991. Included in this amount was depreciation of $5,000, a charge of $6,000 for the amortization of bond discounts, and $4,000 for interest expense. The estimated cash flow for the period is:

A. $66,000

B. $49,000

C. $71,000

D. $65,000

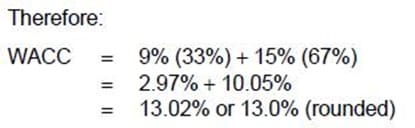

ABC Electric is contemplating new projects for the next year that will require $30,000,000 of new financing. In keeping with its capital structure, ABC plans to use debt and equity financing as follows:

•

Issue $10,000,000 of 20-year bonds at a price of 101.5, with a coupon of 10%, and flotation costs of 2.5% of par value.

•

Use internal funds generated from earnings of $20,000,000.

The equity market is expected to earn 15%. U.S. treasury bonds currently are yielding 9%. The beta coefficient for ABC's common stock is estimated to be .8. ABC is subject to a 40% corporate income tax rate. ABC has a price/earnings ratio of 10, a constant dividend payout ratio of 40%, and an expected growth rate of 12%.

Assume ABC has an after-tax cost of debt of 9% and an after-tax cost of equity of 15%. ABC's weighted average cost of capital is:

A. 11.0%

B. 13.0%

C. 12.0%

D. 11.8%

The net present value method of capital budgeting assumes that cash flows are reinvested at:

A. The risk-free rate.

B. The cost of debt.

C. The rate of return of the project.

D. The discount rate used in the analysis.

Which one of the following would increase the working capital of a firm?

A. Purchase of a new plant financed by a 20-year mortgage.

B. Cash collection of accounts receivable.

C. Payment of a 20-year mortgage payable with cash.

D. Refinancing a short-term note payable with a two-year note payable.

In April 30, 20X4, ABC Corp. approved a plan to dispose of a component of its business. For the period January 1 through April 30, 20X4, the component had revenues of $500,000 and expenses of $800,000. The assets of the component were sold on October 15, 20X4 at a loss. In its income statement for the year ended December 31, 20X4, how should ABC report the component's operations from January 1 to April 30, 20X4?

A. $500,000 and $800,000 should be included with revenues and expenses, respectively, as part of continuing operations.

B. $300,000 should be reported as part of the loss on disposal of a component and included as part of continuing operations.

C. $300,000 should be reported as an extraordinary loss.

D. $300,000 should be reported as a loss from operations of a component and included in loss from discontinued operations.

In single period statements, which of the following should not be reflected as an adjustment to the opening balance of retained earnings?

A. Effect of a failure to provide for uncollectible accounts in the previous period.

B. Effect of a decrease in the estimated useful life of depreciable equipment.

C. Cumulative effect of a change from the percentage of completion to the completed contract method of accounting for long-term construction projects.

D. Cumulative effect of a change from LIFO to FIFO in valuing merchandise inventory.

ABC Corp. has three manufacturing divisions, each of which has been determined to be a reportable segment. In 1989, Clay division had sales of $3,000,000, which was 25% of ABC's total sales, and had operating costs of $1,900,000, as reported to the CFO. In 1989, ABC incurred operating costs of $500,000 that were not directly traceable to any of the divisions. In addition, ABC incurred corporate interest expense of $300,000 in 1989. In reporting segment information, what amount should be shown as Clay's operating profit for 1989?

A. $875,000

B. $900,000

C. $975,000

D. $1,100,000

Home | Contact Us | About Us | FAQ | Guarantee & Policy | Privacy & Policy | Terms & Conditions | How to buy

Copyright © 2026 pass4itsure.com. All Rights Reserved